Trump on a warpath or who needs our scalps

DPRK stated that the complete plan of the attack to Guam will be ready to the middle of August. The minimum of sanity of both sides keeps the market in preventive panic, investors run away in assets without risk. The franc and yen will continue to become stronger to dollar, gold and silver watch up surely.

We read the protocol of FRS (the publication on August 16) especially attentively. We will remind: in accompanying the announcement of FRS from a meeting on July 26 participants of the market paid attention to two aspects: to the assessment of growth of inflation and time of start of reduction of the balance of FRS. As a result of a meeting, the market became more active to sell dollar because of the absence of accurate specifying on the following change of rates in September.

At the moment data confirmed inflation growth deceleration and though separate factors in this process support, Yellen's judgement on the temporality of falling because of specific factors, the purpose on inflation sounded by FRS remains unobtainable in the next months. Analysts think that inflations will accelerate in indices of a month by a month, but leveling of already available extremely feeble data will require 8-12 months. If to suppose that the wave of growth of inflation passed after Trump's victory and taking the office (December-February), then the main growth of inflation in annual indices should be expected not earlier than March 2018.

However, these calculations are not of particular importance as, despite rare curtseys aside Yellen, Trump does not gather leaves her in the second period, and the new head of the Federal Reserve can pursue any other policy pleasing to the White House. Market waitings to increase in a rate at a meeting of FRS in December fell up to 35% on Friday. The current protocol may contain specification on time of start of reduction of balance. Focus on the start of abbreviation of reinvestments in September will cause the growth of profitability of state treasury bills of the USA (and growth of dollar, certainly) even if the reduction will begin with a small volume in $10 billion. Price thorns after the publication of the FRS`s protocol are guaranteed. Investors already aim at Yellen`s announcement at a conference at Jackson Hole on August 24-26.

If the ECB plans to reduce the QE size from the current level of €60 billion to €40 billion that the period when the balance of the ECB will still grow, and the balance of FRS will be already reduced and with acceleration. And this difference will press for EUR/USD until there is a low inflation in EC.

The major factor of influence on currency streams last week hasn't been connected with monetary policy or economic data in any way. Trump has held several meetings on Sunday, a big press conference on Monday is expected. Negotiations between China and Trump continue. According to the insider if don't agree, then statements for the beginning of investigation concerning the theft of intellectual property of the USA by China are possible, it will be explained as the reason for the increase in duties on the export of China and also the possible introduction of additional sanctions.

However, the majority of currencies wait for the reaction of China. The growing tension between the USA and North Korea has already caused the collapse of USD/JPY. Deterioration appetite to risk, the closing of large positions of carry with traders and outflow of investments, have already struck a serious blow to the Canadian, Australian and New Zealand dollars. If China remains neutral, but won't become reserved to support North Korea, yen, Aussie and Kiwis will react much more quietly, than in a situation of full coordination of the Chinese position with Trump.

Apparently, the chancellor of the treasury of Great Britain Hammond and the minister of international trade Fox who were accused of the attempt of failure of Brexit have buried the hatchet, having made a joint statement that now Britain has nothing to do in the EU. BoE convinces again that increase in a rate remains possible with a further growth of inflation and at signs of acceleration of growth of the economy. On August 18 the second stage of negotiations on Brexit opens, the amount of financial compensation of Britain for an exit from the EU will be the main subject.

Aggravation of a geopolitical situation leads to escape from risk, that is euro can be considered as a funding currency for some time. However, any new negative information on Mueller's investigation against Trump or concerning postponement of ratification of tax reform for 2018 will cause updating of maxima on eurodollar. We don't lose sight of EUR/CHF − euro grows almost vertically on interventions of SNB, completely ignoring the base.

From other news we will note:

- EIA has raised the forecast of an increase in demand for 2017 to 1,5 million barrel/day in respect with this, as expected, the global surplus has to decrease, despite an increase in production in North America and weak implementation of agreements of OPEC (in July – only 75%). It is also stated decrease in stocks in industrialized countries in June and July. On August 11 there have taken place negotiations concerning the reduction of oil production between ministers of oil of Saudi Arabia and Iraq. We expect the official statement today.

- Last week demand for black gold from China sharply decreased, as a result, import of crude oil collapsed to a minimum in seven months. It can be connected to seasonal factors, therefore, most of the analysts do not hurry with outputs. Morning data on China were released mixed: retails showed growth by 10.4%, industrial output also increased but is more feeble than the forecast. Raw currencies can go to defense.

- There is no almost information from the ECB − Draghi forbade members of the ECB to comment on the forthcoming changes in a policy, expecting that the market itself gradually will see reason. The publication of the protocol of the ECB on Thursday may contain hints on entering of some serious amendments to financial policy (backdating!) for force depreciation of euro.

The current week the main data on the USA will be retails, the production index of FRB of Philadelphia, a research of moods of consumers from Michigan; in the EU – the report on inflation (change isn't expected) and GDP growth for the 2nd. The package of important data of Britain will exert considerable impact on dynamics of the pound: analysis of the growth of inflation, report on the labor market and retails. Be careful, speculators on the main tools, including raw, strenuously become more active.

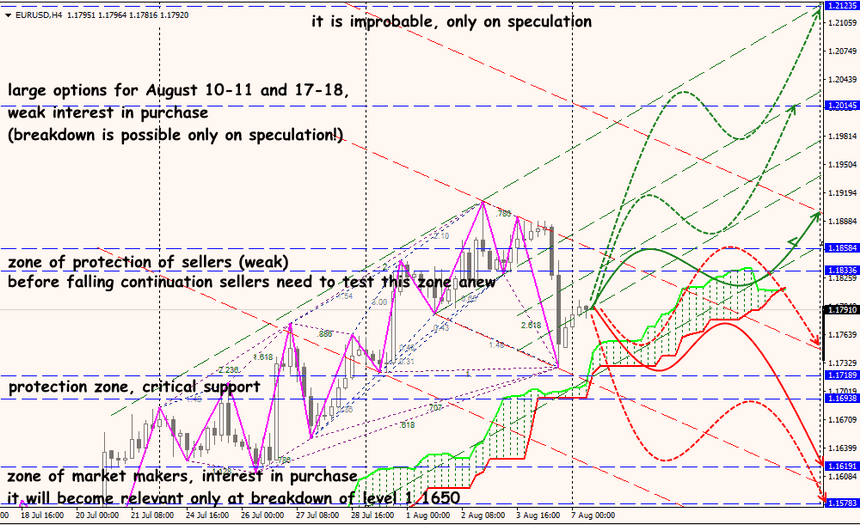

Technical Analysis EUR/USD

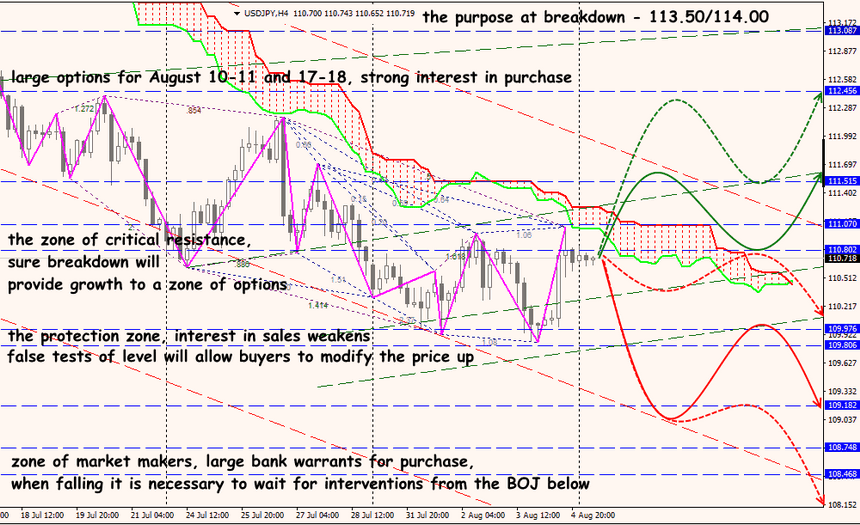

Technical Analysis USD/JPY